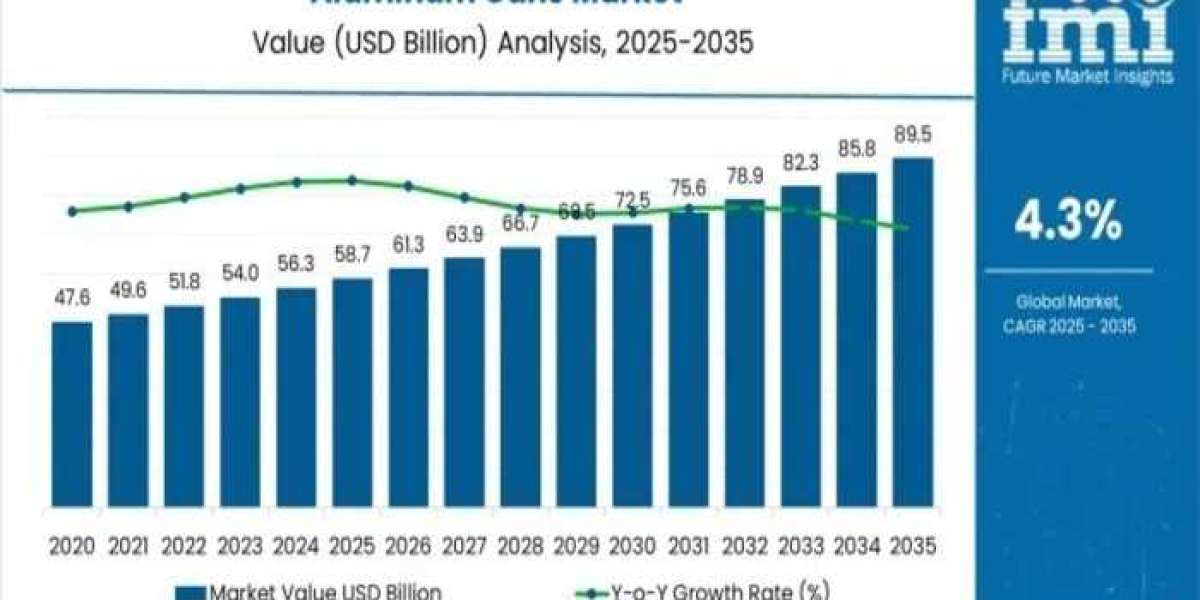

The global aluminum cans market, valued at USD 58.7 billion in 2025, is projected to reach USD 89.5 billion by 2035, expanding at a steady CAGR of 4.3%. The industry stands at the forefront of a transformative decade that will redefine how beverages are packaged, chilled, and consumed across the world. From carbonated soft drinks and beer to energy drinks and ready-to-drink (RTD) beverages, aluminum cans continue to set the gold standard for lightweight, portable, and recyclable beverage packaging.

From 2030 to 2035, the market will further climb from USD 72.5 billion to USD 89.5 billion, adding USD 16.8 billion in value and accounting for 58% of decade-long growth. This second phase will be marked by the mainstream integration of specialized can formats, greater compatibility with high-speed filling lines, and a shift toward multi-beverage aluminum systems optimized for soft drinks, craft beer, and functional beverages alike.

Uncover the Massive Potential of the Edtech Market – Get Our Sample Report Now

https://www.futuremarketinsights.com/reports/sample/rep-gb-4434

Europe Leads with Beverage Innovation and Recycling Efficiency

Europe represents one of the most mature and forward-thinking aluminum can markets globally, projected to grow from USD 16.4 billion in 2025 to USD 24.2 billion by 2035, at a CAGR of 3.9%. With long-standing expertise in beverage packaging, European producers are setting global benchmarks in recyclability, material recovery systems, and deposit return compliance.

Germany continues to lead the regional landscape, accounting for over 32% of Europe’s market share in 2025, supported by its robust brewing traditions and precision manufacturing. The United Kingdom, driven by a vibrant energy drink and craft beer ecosystem, follows closely with 25% share, while France, Spain, and Italy maintain strong performance through premium beverage packaging applications.

Europe’s aluminum can producers, such as Ball Corporation and Ardagh Group, are investing in lightweighting technologies and digital printing systems that enhance branding opportunities without compromising material efficiency. This shift aligns with the continent’s sustainability mandates and consumer expectations for eco-friendly, high-quality packaging.

Market Segmentation Highlights

- By Can Type: The standard 12 oz can continues to dominate, representing nearly half (48%) of total demand in 2025. These cans remain the backbone of beverage packaging due to their universal compatibility with existing filling lines, optimal chilling capability, and cost efficiency.

- By Application: Carbonated soft drinks lead the aluminum can market, accounting for 41% share in 2025. The segment thrives on single-serve beverage trends, cold chain distribution, and vending channel growth across Europe’s retail ecosystem. Meanwhile, energy drinks, craft beer, and ready-to-drink cocktails are emerging as high-value niches due to premiumization and lifestyle-driven demand.

Innovation Pathways: The Next Wave of Growth

The decade ahead presents a wide spectrum of growth opportunities for aluminum can manufacturers and beverage companies alike:

- Energy Functional Beverages – Enhanced barrier coatings and resealable designs catering to high-performance drink categories.

- Craft Beer Premium Alcohol – Specialty cans supporting nitrogen dosing, limited-edition branding, and taproom compatibility.

- Slim Sleek Formats – 8.4 oz and 250ml designs aligning with portion control and fashion-driven aesthetics.

- Advanced Graphics Smart Printing – Thermochromic inks, QR-linked storytelling, and tactile finishes driving brand engagement.

These pathways together could unlock USD 60–70 billion in incremental value globally by 2035, with Europe expected to capture a significant portion due to its design innovation and recycling leadership.

Drivers and Challenges

Growth Drivers:

- Rising demand for sustainable packaging that aligns with circular economy goals

- Expansion of convenience retail and vending machine channels

- Increasing preference for ready-to-drink formats among urban consumers

- Continuous advancements in barrier coatings and printing technologies

Challenges:

- Aluminum price volatility, impacting input costs and profit margins

- Capital-intensive production and coating uniformity requirements

- Competition from plastic and glass packaging alternatives in price-sensitive markets

Competitive Landscape

The global aluminum cans market remains moderately consolidated, with 18–25 key players controlling nearly 55% of global share. Industry leaders such as Ball Corporation, Crown Holdings, and Ardagh Group dominate through vast production capacity, RD investment, and long-standing relationships with beverage giants.

Emerging players including CANPACK and Showa Aluminum Can Corporation — are gaining traction with specialty formats, lightweight designs, and eco-friendly coatings tailored to new-age beverage categories.

Why FMI: https://www.futuremarketinsights.com/why-fmi

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.